Heat treatment market in CZ and SK

Last June I published the first numbers of my statistics. I took into account all heat treatment operations known to me, including PVD and Laser, both typically commercial and typically in-house, and in between the so-called hybrid, where the in-house heat treatment plant provides part of the capacity to the free market.

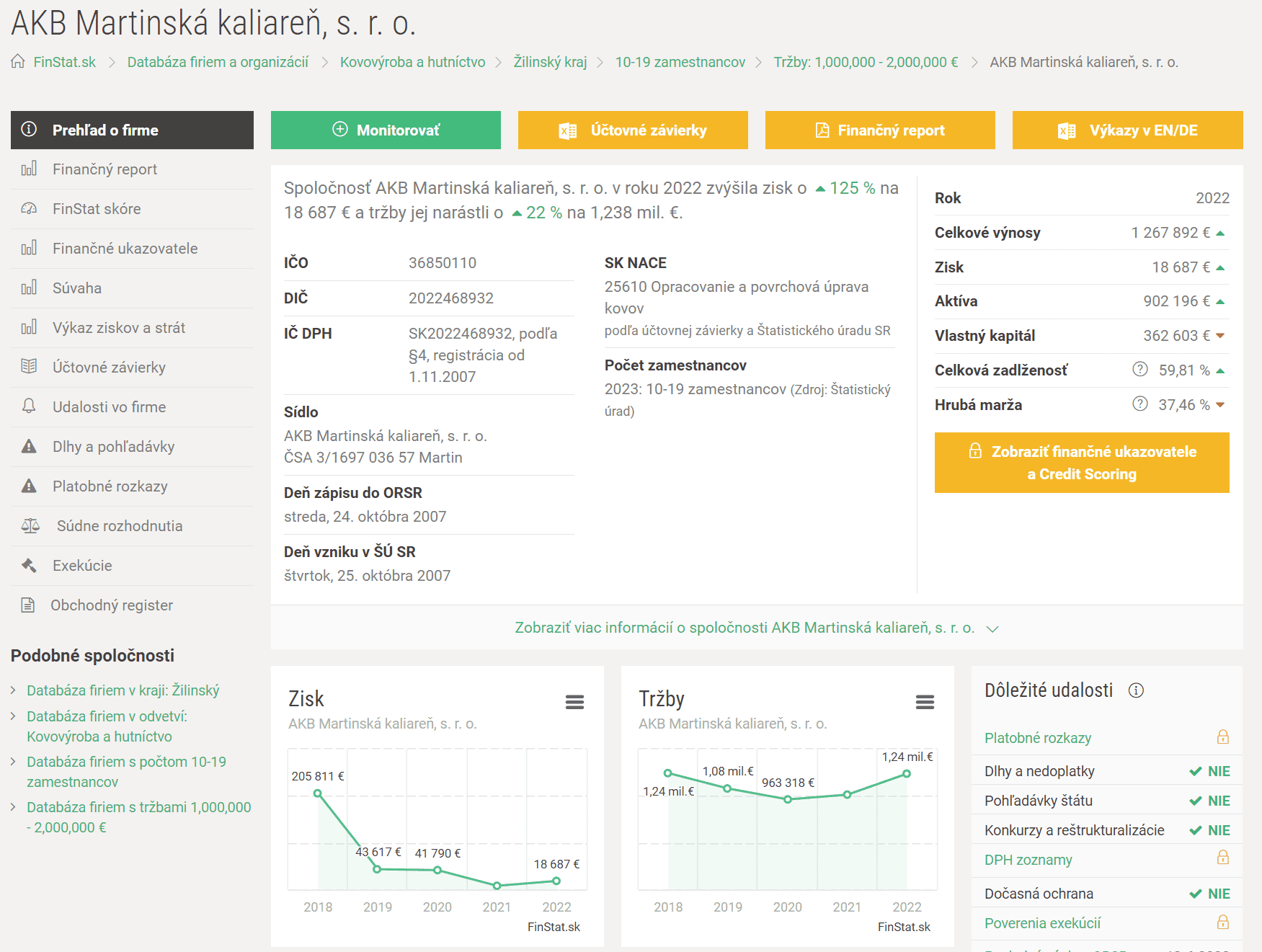

It is a big omen, because only commercial companies have figures on the sale of thermal processing in their financial statements. For others, this is a very rough estimate. The second problem is that in CZ there is an obligation to publish data in the Commercial Register, but for small companies this only applies in a shortened version. That’s why many commercial heat treaters only have a balance sheet in Business register, not a Profit and loss statement. In Slovakia, the situation is significantly better, because the data is transmitted in a uniform and complete electronic form, and it is not a problem to have the data immediately up-to-date: https://finstat.sk/, see e.g. the statement below.

Fig. 1 – Record example from Finstat.sk

So, everything needs to be taken with a grain of salt and if you have better resources, then don’t look at this. The total market is roughly 5.3 billion CZK. It has grown by 2 billion since my last presentation, but that’s just by supplementing my list with newly found and added entities. Big changes are likely to follow, for example, it is already officially published on The Monty.com that the Hyundai heat treatment shop in Nošovice is for sale, a similar fate befell Šroubárna Turnov.

Fig. 2 – Hyundai equipment in Nošovice, 4 roller high-capacity furnaces from the company Dongwoo, year of manufacture 2007 – the Monty.com, 12/12/2023

Roughly 43% are covered by purely commercial heat treaters, 4% hybrid and purely in-house 53%. These numbers alone show that there is a mistake somewhere, because commercial heat treaters usually have around 20% of the market, the rest is on the so-called captive. But it is very difficult to appreciate the performance of in-house heat treatment operations when we only have vague ideas about them. This ratio has not changed much from my originally published data.

Fig. 3 – Estimated market share of commercial, hybrid and in-house heat treatment plant in CZ and SK

From the point of view of purely commercial heat treaters, I register 28 of them, the situation is as follows. Overall, they have a market share of CZK 1.58 billion. Of course, Bodycote is at the top, while Vlkanová (SK) and Praha (CZ) are also at the top in terms of total turnover. It is only after them that Galvamet, Kaliareň Považská Bystrica and Vakuová kálírna Meduna appear. The market share of Voestalpine in Vyškov and Martin, as well as Swiss Steel in Hustopeče, is also a secret. We cannot find the exact numbers, they are hidden somewhere in the total sales, i.e. they are listed with the sale of steel.

Fig. 4 – TOP 28 of heat treaters in CZ and SK

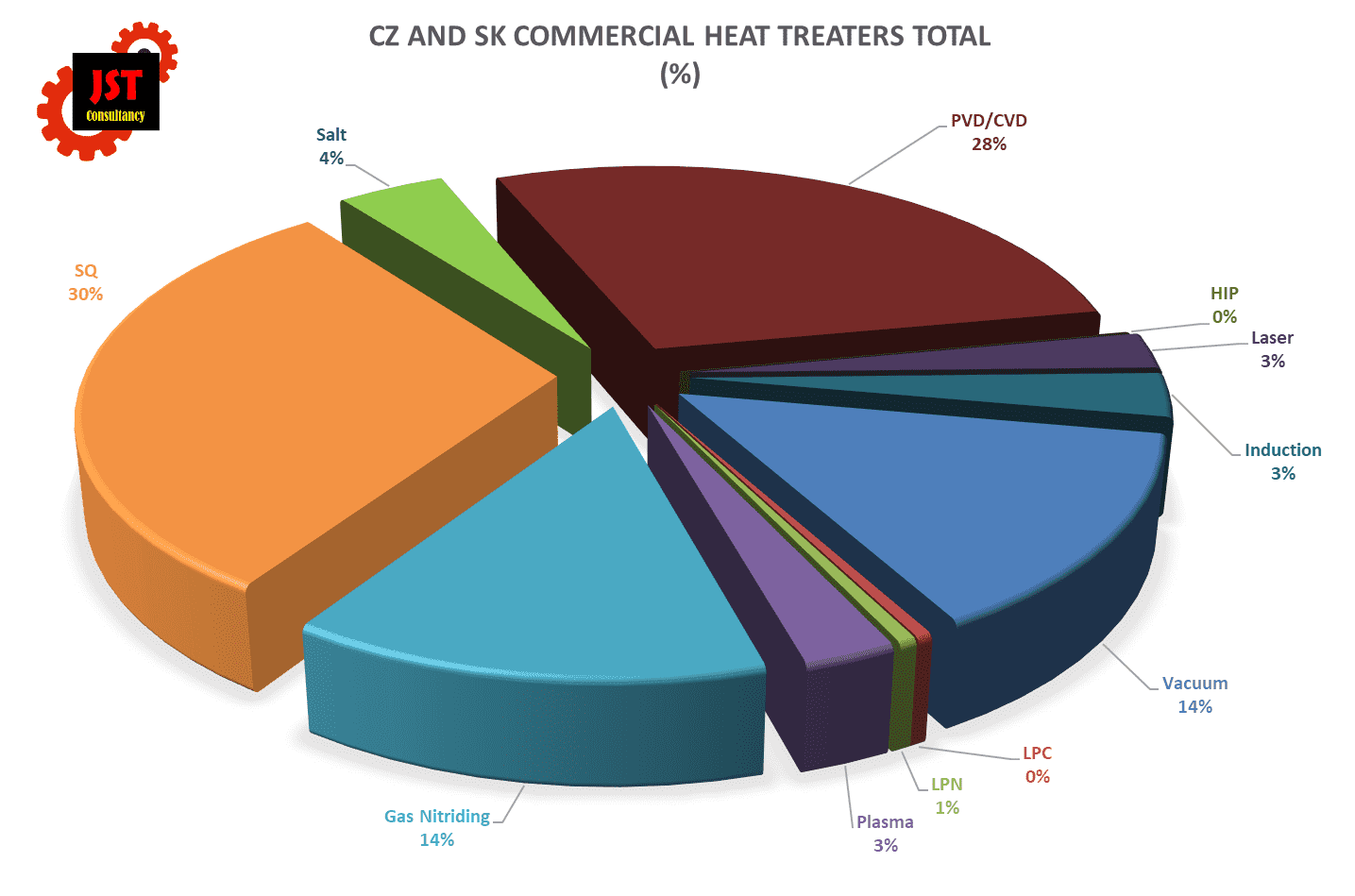

According to the individual technologies, the situation is as follows. I only take into account commercial heat treaters or surface treatments, where the situation is clearer. PVD/CVD technology accounts for a large share. This is surprising, but it also shows that this is an expensive technology, with very well applied added value. In kilogram terms, of course, this technology cannot compete, for example, with heat treatment in multi-purpose furnaces.

In terms of classical heat treatment, SQ continues to dominate, followed by gas nitriding/nitrocarburizing and vacuum. The position of LPC, where we are within 1%, is surprising. This technology is very well represented in in-house heat treatment operations thanks to the ECM lines in Bosch Jihlava and Poclain Hydraulics, or by ALD in Škoda-Auto Mladá Boleslav and Vrchlabí. But it’s worse for commercial heat treaters, investing in a 15 bar furnace from SecoWarwick does not allow the transition from SQ to LPC, and therefore these furnaces are mostly used for standard gas quenching, not for low-pressure carburizing.

Fig. 5 – Share of individual technologies on the commercial market

And what can be expected in the near future? Above all, the fight for energy will begin. Their share of the costs is growing and will be additionally burdened with additional taxes within the framework of the EU policy FIT55. Electromobility is also related to this, and there it is clear that 30% of steel, heat-treated parts will be removed from our circulation. However, since electromobility is related to the concept of GIGA factors, the consumption of aluminium will increase and the related increase in the need for GIGA die-casting tools. There will therefore be a search for large furnaces, up to 10 tons of hardening capacity.

The effort will be to replace classic SQ furnaces with vacuum furnaces, whether with two, three, or more chambers, where we can get from the current energy consumption of 1-2 kWh/kg to 0,5 kWh/kg. And although Ipsen is working on the development of a hybrid SQ furnace, heated by electricity or hydrogen, this technology will only make sense after 2030, when green hydrogen will be available in sufficient quantities and at an affordable price.

In connection with the EURO 7 emission standard, the demand for nitrocarburizing will increase, but it will be necessary to solve the same energy problem as with multi-purpose furnaces. The existing single-chamber furnaces will have to be replaced with more efficient devices. E.g. NITREX already offers continuous lines for nitrocarburizing of brake discs, and ECM offers the Flex system with up to 10 FNC chambers.

And what about LPC? Any type of steel can be carburized under reduced pressure. But the trend will be to replace expensive, alloyed steels with material with a minimum of alloying elements. However, they cannot be mass-processed with nitrogen overpressure quenching, oil quenching is required. Therefore, the need for two and multi-chamber solutions with oil hardening will increase. Development and innovation in the field of washing will also be related to this.

According to Janusz Kowalewski from Ipsen Asia, it is also necessary to take into account other trends in the field.

- In the case of commercial heat treatment, there will be further consolidation into the larger units

- The development of digitization will increase in order to simplify and automate the heat treatment operation

- It can be expected that there will be a transfer of know-how and responsibility in the area of the heat treatment process and maintenance from the end user to the furnace manufacturer using software solutions such as Ipsen PdMetrics

- Furnaces with a high CO2 content will be gradually replaced by more efficient vacuum systems, but their size will be limited by flexibility requirements

- There will be an increase in popularity of processes with lower temperatures or shorter cycle times

So, I wish you a successful year 2024

Jiří Stanislav

3. ledna 2024